AI's impact on personal finance management

Making better financial decisions with AI!

According to Debt.org, an average American household has $8,398 of credit card debt, and the current inflationary environment and layoffs have not been helping to reduce this debt. However, there is no doubt a personal financial assistant can help people manage their finances by steering them in the right direction to save or invest money.

Generative AI and AI Agents will significantly improve Personal Finance Management (PMF) products and, as a result, will unlock new use cases. Using AI in this space is nothing new. Robo-advisors such as Nutmeg and Personal Capital have been helping tech-savvy folks make intelligent decisions about investing, taxes, etc., using machine learning algorithms. However, Generative AI has added a new dimension to accelerate the personal finance industry forward by integrating the conversational aspect of human interaction into the financial decision-making process. AI technology has the potential to revolutionize personal finance by enabling advanced algorithms to analyze vast amounts of financial data, provide personalized recommendations, and automate spending and savings.

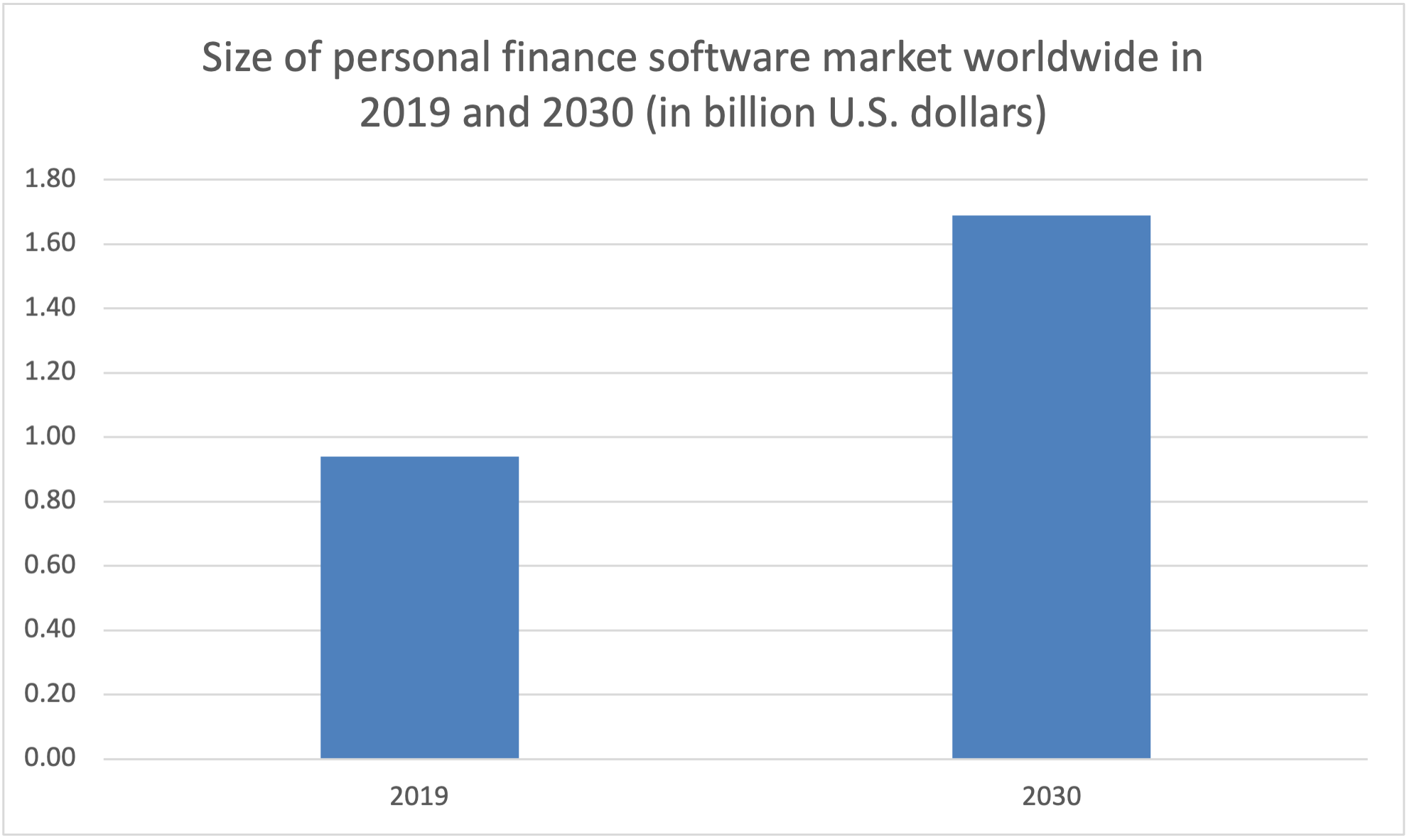

The Personal Finance software market is already in a strong position and is expected to grow at a CAGR of 5.7% between 2019 and 2030. However, given the current AI wave, these products are poised to get a magnitude better by competition in the market and to gain newly minted debt-conscious millennials and GenZs who want to manage their finances better.

One of the primary sources of change in the personal finance management software market will be fueled by the shift in digital banking products. As more and more people transition to digital banking, spending more time on their banking app or website, companies will be incentivized to integrate customized financial betterment products in their existing services.

NerdWallet has been around for some time, advising people seeking financial services. Whether taking a loan or getting a new credit card, NerdWallet will refer you to third-party products, earning a commission from these providers. NerdWallet pulled in $169.6 million in revenue in Q1 ‘23, growing at +31% YoY with 23 million average Monthly Unique Users (MUU). This is an excellent sign for the personal finance industry’s growth. People want to be informed and make sound financial decisions.

The introduction of Generative AI tech and AI agents will only make personal finance products better and faster. Let’s look at the companies that seem to be integrating AI with their existing products.

Current players integrating AI-wave 🌊

1. Parthean AI

Parthean AI aims to be your financial coach. Building upon its existing offerings of finance educational videos, Parthean AI integrates a conversational AI to enable users to ask questions. You can ask, for example, “How much can I afford to spend on my next vacation?” or “How much money do I need to start saving to buy a house in the next three years”?. The fact that you can link your bank accounts with the app makes it easier for the app to check your financial inflows and outflows and provide recommendations based on data.

I downloaded the app's free version to get a feel for its AI. This feels like interacting with ChatGPT, but Parthean’s ability to train the recommendations based on your financial data makes it customized for your needs. Here is what I asked:

2. Wallet.AI

Wallet.AI’s founding (2012) predates the current Generative AI explosion. The product is not yet launched, and its positioning is still vague, but based on the few articles I could find about the product, here is what I understand it might do. It will look at spending signals from all of your activities, such as you buying stuff from an Instagram ad, you getting a coffee from Starbucks, etc. And based on your income and budget, it will tell you whether you should buy that t-shirt you have been eyeing. What I found interesting about Wallet.AI’s initial positioning based on this old article is that the product would be offered to financial institutions. The initial pitch seems that the banks would integrate Wallet.AI into their customer accounts, enabling end users to make intelligent financial decisions. As a result, Wallet.AI would charge the financial institutions rendering its services instead of the end customers. I don’t know how much that would go against banks’ incentives, but we will find out when the product launches.

3. OpenAI’s ChatGPT

Of course, we cannot miss ChatGPT if we discuss integrating Generative AI in PMF apps. I decided to ask ChatGPT how much I can afford to pay in my monthly car payment if I make a $14K monthly gross income. Check out this thorough and nuanced response. It took a conservative approach of putting 10% of my monthly income towards a car and considered the maintenance and insurance - like a solid personal financial advisor would.

4. JPMorgan/Bloomberg

Big Banks have already been utilizing Financial robo-advisors, automated investment platforms that use algorithms and technology to provide personalized financial advice and manage portfolios. Mostly, it tends to be a hybrid model where robo-advisors provide rudimentary advice, and then an actual human jumps on the call for a more detailed discussion. But this model changes with the introduction of Large Language Models (LLMs). All banks realize this tectonic shift in technology. However, JPMorgan and Bloomberg are the first banks to publicly announce that they are working on IndexGPT and BloombergGPT, respectively.

5. Intuit

Intuit recently announced the launch of a suite of Generative AI products that will help its customers make smarter decisions when filing taxes, managing cash flows, etc. Additionally, as part of their overall GenOS launch, Intuit has announced the launch of developer platforms and UX frameworks to give a push to Generative AI development on the Intuit platform. Intuit owns Credit Karma, QuickBooks, Mailchimp, and TurboTax, and this broad selection of products under one umbrella makes it easier for Intuit to scale its generative AI capabilities and train on a vast amount of data.

What’s next? 🚀

Proactive financial actions rather than reactive advice

I see an ample opportunity in a space where you don’t have to ask your personal financial advisor whether you should buy X or Y. I would want my financial advisor to take proactive action and then explain why it made the decision it did. For example, if I have a streaming service I have not used in three months, I want my AI agent to go ahead and cancel the service. I would much rather get a notification that my infrequently used streaming service has been canceled than ask my AI agent whether I should cancel it.

Fueled by subscriptions and free trials, we are used to new purchasing subscriptions every day. Most people do not keep track of how many subscriptions they have, let alone take the time out of their day to ask a piece of software whether they should cancel an X subscription. Products will set up a budget to do the most critical things based on my income, and my advisor can automatically block or allow purchases.

Always on AI-powered passive investors

I sense that startups will develop products that can make passive investments for me to generate higher returns. Products that, in addition to scanning my bank account statements, will also monitor multiple financial offerings out there and open new accounts, and even move funds. For example, suppose my money is sitting in a 0.01% interest rate check or savings account in X bank. In that case, I want my financial advisor to find different banks that provide a higher interest rate and proactively prompt me to open a new account and move my money to the new account that pays higher interest.

Fully automated budgeting

There are a million budgeting tools out there. YNAB, Mint, Honeydue, etc. While these tools work great after manually assigning your budget to each activity, these are also very time-consuming to set up and keep track of. Without generalizing too much about these apps, I sense that these apps will be hugely improved by introducing AI agents that can update your monthly or yearly budgets based on spending signals and income fluctuation. For example, if my income shrank or expanded, my budget will automatically be updated based on how I have spent my money historically. For example, I want my budgeting app to read my bank transactions and automatically assign each spend within a specific category. And if, for instance, my expenditure in the “going out” category is less this month than the last, I want that excess money to be budgeted under a different category, for example, “gifts.” Dynamic budgeting, or set and forget it, will be a table-stake in most budgeting apps.

Customized reporting in your budgeting apps

With the help of Generative AI, creating customized reporting based on user-entered queries will become a norm. In addition to budgeting, users will demand state-of-the-art metrics and spending analysis. If the personal finance companies do not develop their own LLM software, they would most likely partner with third parties such as Writer AI to bring on-demand customized reporting to stay ahead of the competition. Do you want to create a spending forecast report for a week? GenAI integration will quickly look at your data and create pretty graphs for you to look at.