Data centers defying the commercial real estate downturn 🏢

If you are following any news about commercial real estate, you know there is doom and gloom about how it will collapse under the burden of loan maturity dates. Even Blackstone, the world’s largest alternative asset manager, was dragged into the bad news about the market’s dangers. There is, however, a different side of commercial real estate, which is not feeling the same pain as the corporate office buildings. And that is the data center segment.

The massive shift to the cloud, 5G rollout, AI/ML, and High-Performance Compute (HPC) are some growth drivers behind the data center boom. Major technology companies like Amazon, Microsoft, and Google are investing billions to build new data centers to keep up with demand. Colocation providers are also expanding as more enterprises move their data off-site to third-party facilities. The resilience of the data center business comes from its essential role in the digital economy. As more activity moves online due to hybrid work arrangements and digital transformation initiatives, data center space is more crucial than ever. While some parts of commercial real estate may decline, data centers will likely see sustained demand growth for the foreseeable future.

As per this Upsite’s report, 25 million square feet of data center capacity was added in 2022, on top of 250 million square feet of already existing data center capacity worldwide. This includes growth in colocations, hyperscalers, and enterprise data centers. Understanding the business, environmental, and geopolitical drivers behind this growth is helpful.

Digital Existence: this applies to virtually everyone, from individuals to big corporations. Taking this one step further, the digital presence has to be localized and personalized to make it relevant for consumers. This increases the need for infrastructure that can support localization and be ready to serve consumers’ web traffic.

Business-to-Business (B2B) transactions: inter-organization data consumption is rising thanks to specialized data providers and disparate systems. This increases the need for companies to connect data sources with their consumers, driving the market for interconnections and data centers that can support massive data exchanges.

Data vicinity: Employees and consumers demand faster and more localized experiences relevant to them. This increases the need to deploy more edge infrastructure than ever. For example, Australian employees don’t want to get served web traffic meant for the US workers, and they want to access the content they are interested in faster than ever. This gives rise to edge infrastructure deployment, removing the need for a few central servers to handle the traffic.

ESG is still top of mind for companies: 90% of the executives believe that companies need sustainability as one of their operating goals, and IT is a critical part of achieving the ESG goal. In a digital economy where servers and data centers have become commodities, efficiently utilizing power and space to build a physical presence is necessary. This requires novel approaches to rebuilding data centers.

These developments are increasing the demand for companies that provide interconnections, private data exchange, hyperscalers, and data centers to enable instant and seamless interactions across the globe. GXI reports that personal interconnection capacity is expected to grow at a 40% compound rate by 2025, reaching more than 27 Terabits per second of data exchanged annually.

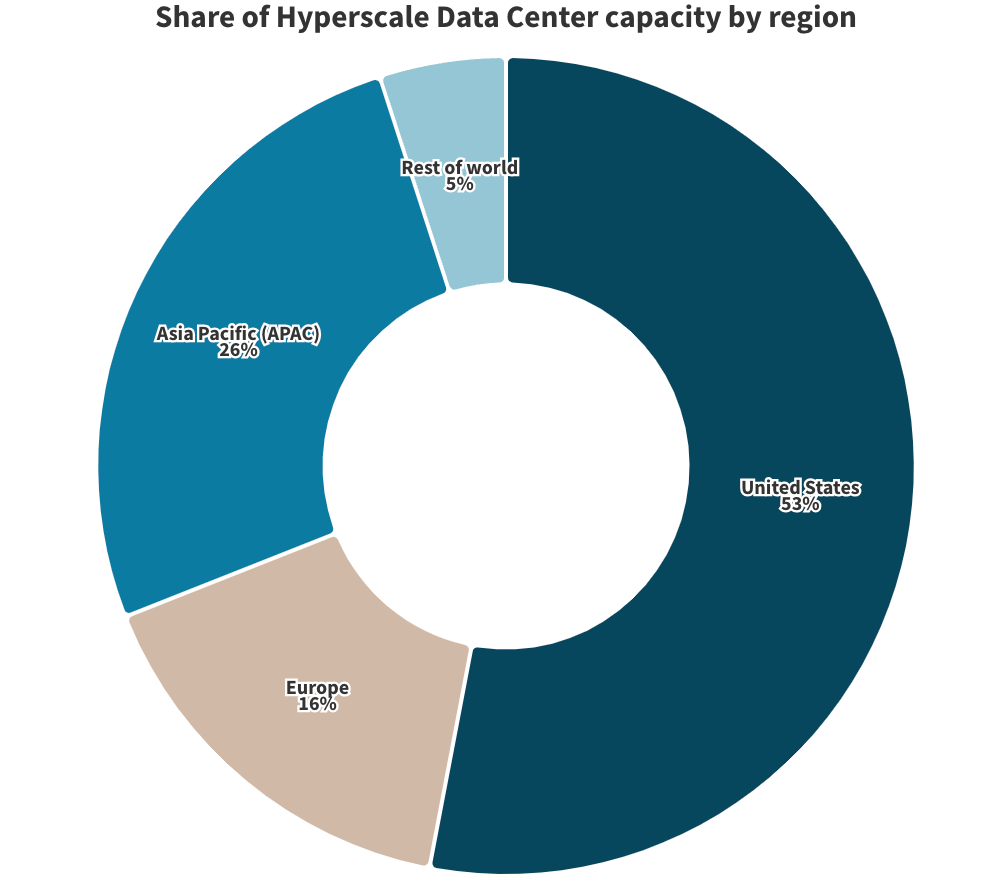

While North America leads the total share of hyperscalers data centers, I think the next leg of the growth will likely come from Asia Pacific and Latin America, given the population growth and the digitalization in the regions.

Public companies running data centers and interconnection exchanges, such as Equinix and Digital Realty, invest heavily in Asia and Non-US regions. In the past week, Digital Realty, an Austin-based firm, signed a deal with Reliance Jio and Brookfield Infrastructure to build data centers in Indian metro areas, drawing $122M of investment from the Indian conglomerate. Similarly, last month, EdgeConnex announced a joint venture with Adani to build more data centers in India, planning to invest as much as $213M. LaTam is not behind in drawing data center investments either. The region is expected to attract $1.8B in data center investment from Equnix, ODATA, Ascenty, etc. between 2023 and 2028. Lastly, Africa is also attracting big dollars from data center operators. For example, in 2022, Equnix closed on its $278.4 million acquisition of Africa’s interconnection provider, MainOne.

Artificial Intelligence, Machine Learning, and Analytics are driving record revenue for AI chip makers like NVIDIA. As more and more companies use AI chips, more capacity will be needed to house these machines in data centers. NVIDIA reported record revenue in Q1 ‘23 from its Data Center business — $3.75 billion, up 83% from a year ago. I believe the increase in AI hardware consumption has a trickle-down effect on data center builders, and this trend will only accelerate as more players fine-tune their AI hardware (think AMD, Intel, etc.)